Go figure. The circumstance is a lot more complex, so consider this is an initial lesson on a really intricate topic. Idea: Home loan rates can increase really quickly, however are typically decreased in a slow, calculated way to secure home loan lenders from rapid market shifts (what is the current interest rate for home mortgages). That very low marketed home mortgage rate sure appearances goodBut be sure to examine out the great printYou most likely have to be an A+ borrowerAnd you might need to pay discount rate points tooAlso note that the par rate you see promoted on TV and the web often do not take into consideration any home loan rates changes or costs that could drive your actual interest up substantially.

If your deposit or credit history isn't that high, or your home equity is low, your home mortgage rate might sneak greater too. Occupancy and home type will likewise drive rates higher, assuming it's a 2nd home, financial investment home, and/or a multi-unit home (who has the best interest rates on mortgages). So expect to pay more if that holds true.

There are also loan amount restrictionspricing can alter depending on if the home mortgage is conforming or jumbo. Generally, regular monthly payments are higher on the latter, all else being equivalent. To put http://rylanegwa676.image-perth.org/excitement-about-how-do-reverse-mortgages-work-when-you-die it simply, YOU and your residential or commercial property matter too. A lot!If you're a dangerous customer, at least in the eyes of prospective home loan loan providers, your mortgage rate may not be as low as what you see promoted.

At the borrower level, the biggest consider determining the price of a home mortgage is generally credit rating. One of the most essential factors that you can control is your credit rating, so if you can at least get a handle on that and work to keep your scores above 760, your prices ought to be optimal, all else being equivalent.

There are loan calculators that will tell if paying points make good sense depending upon your circumstance, the length of time you prepare to remain in the house, and so on. Rates can also differ significantly based upon how much a certain lender charges to originate your loan. So the last rate can be controlled by both you and your loan provider, despite what the going rate happens to be.

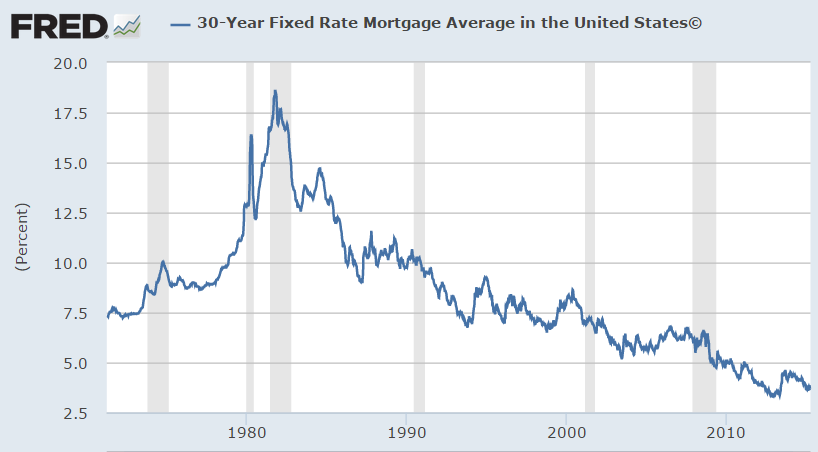

Finally, note that there are a variety of various loan programs offered with different interest rates. Are we discussing a 30-year set rate or an adjustable-rate mortgage, the latter of which will have a lower rates of interest. Loan type and loan quantities can Check out the post right here play a big function here. Below are Freddie Mac's, updated weekly every Thursday early morning.

The Buzz on What Happens To Mortgages In Economic Collapse

The information is collected Monday through Wednesday, so they aren't necessarily going to match up with today's mortgage rates if rates increased or fell from then up until now. Consider this a starting point:30- Year Fixed * 2. 71% 2. 71% 3. 73% 15-Year Fixed * 2. 26% 2. 26% 3. 19% 5/1 ARM2. 79% 2. 86% 3. 36%- Mortgage rates are presently trending -* symbolizes a record lowSince 1971, Freddie Mac has carried out a weekly survey of consumer mortgage rates.

These averages don't use to federal government home mortgage like VA loans or an FHA mortgage. The numbers are based upon quotes provided to "prime" borrowers, those with high credit report, suggesting best-case pricing for the many part. I think the residential or commercial property key in Click here! the survey is for a one-unit primary home too, so anticipate a rate rise if it's a holiday home or rental residential or commercial property, or multi-unit home.

To put it simply, your mortgage rate may deviate from the national average for any number of reasons, however if your home loan is quite run of the mill, you might expect rates to be similar. As you can see, 30-year fixed mortgage rates are the most expensive relative to the 15-year fixed and select variable-rate mortgages.

So you pay a premium for the stability and absence of threat, and the opportunity to re-finance if rates occur to go down. Rates on the 15-year repaired are substantially more affordable, however you get half the time to pay it off, implying bigger regular monthly payments and a lot less interest paid.

25%) below the 30-year repaired. The much shorter term suggests you'll likewise conserve a heap on interest. Rates on ARMs are discounted at the beginning since you just get a limited set period prior to they become adjustable, at which point they usually rise. Grab a home loan calculator and price out different loan types to see what makes one of the most sense for your circumstance.

If your specific loan situation is higher danger, whether it's a greater LTV and/or a lower credit report, it will most likely be priced higher. If you're trying to find present mortgage interest rates, you can take a gander at these weekly averages to see both the direction of rates and the ballpark figures to at least get an estimate of what you might get at any offered time.

The Single Strategy To Use For What Is An Underwriter In Mortgages

71% per Freddie MacPreviously it had been as low as 2. 72% during the week ended November 25th, 2020The 15-year fixed also hit its lowest level of 2. 26% on December 3rd, 2020During the week ending December 3rd, 2020, 30-year set mortgage rates struck new all-time lows. The popular 30-year repaired was up to 2.

72%, per Freddie Mac, the most affordable point given that tracking began all the method back in 1971. Formerly, it had actually been as low as 2. 72% throughout the week ended November 25th, 2020. Up until now, there have actually been 14 brand-new record lows set for mortgage rates in 2020. The 15-year fixed hit a record low of 2.

It had actually formerly been as low as 2. 28% during the week ended November 25th, 2020. Its floor was 2. 56% during the week ended May second, 2013 before reaching these recent new lowest levels numerous times in 2020. Throughout the same week back in 2013, the $15/1 ARM also hit its all-time record low of 2.

Lastly, the 1 year ARM fell to 2. 41% during the week ended April 10, 2014, its floor on record considering that 1984. Many financial experts do not see rates falling back to these lows again, though anything is possible if the economy warrants such a relocation. Spoiler alert, rates struck new lows!Wondering if home mortgage rates are going up or down in 2020 and the year after? Wonder no longer.

Take them with a grain of salt due to the fact that they're not necessarily precise, simply forecasts for future rate movement. Fannie Mae3. 6% 3. 6% 3. 6% 3. 5% 3. 6% Freddie Mac3. 8% 3. 8% 3. 8% 3. 8% 3. 8% MBA3. 7% 3. 7% 3. 7% 3. 7% 3. 8% NAR3. 7% 3. 7% 3. 8% 3. 8% 4. 0% As you can see, mortgage rates are predicted to remain low in 2020.

Naturally, it will differ slightly depending upon which forecast you think. Mortgage rates are anticipated to stay in the mid-to-high 3% world in 2020, which need to be welcome news to most. I have actually simply launched 2020 mortgage rate forecasts for those trying to find a more in-depth evaluation. Find out more: What home mortgage rate can I anticipate!.

Unknown Facts About What Is A Gift Letter For Mortgages

?.!?. NOTIFICATION: This is not a commitment to lend or extend credit. Conditions and restrictions might use. All home lending items, consisting of home mortgage, house equity loans and home equity credit lines, go through credit and collateral approval. Not all house financing products are offered in all states. Hazard insurance and, if appropriate, flood insurance coverage are needed on security property.